When deciding how much house you can afford, it’s crucial to determine if a home fits into your monthly budget. A mortgage calculator helps you understand the monthly cost of a home. Our calculator allows you to enter different down payments and interest rates to help determine what is affordable for you.

Lenders determine how much you can afford for a monthly housing payment by calculating your debt-to-income ratio (DTI). The maximum DTI to qualify for most mortgage loans is usually between 45-50%, including your anticipated housing costs.

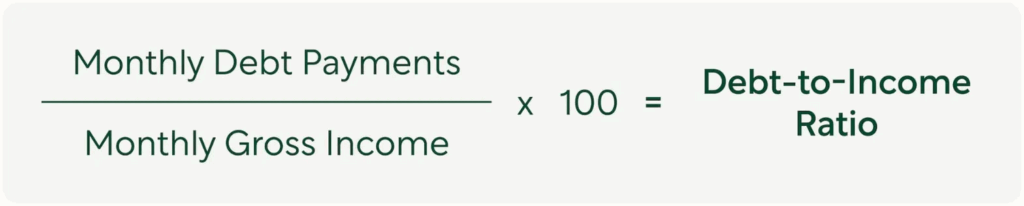

Your DTI is the balance between your income and debt. It helps lenders assess the risk of approving your loan. The DTI ratio shows how much of your gross monthly income goes to creditors versus how much is left as disposable income. It’s typically expressed as a percentage. For example, if half of your monthly income goes to debt payments, your DTI is 50%.

Formula for calculating your debt-to-income (DTI) ratio:

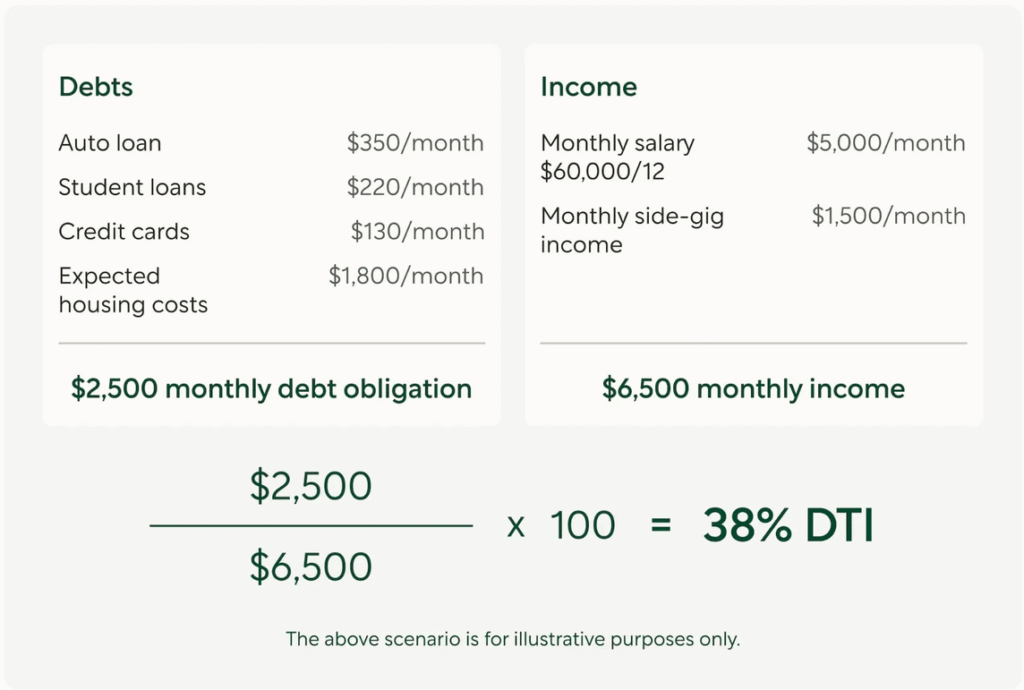

Here’s an example of what calculating your DTI might look like:

Your monthly mortgage payment includes loan principal and interest, property taxes, homeowners insurance, and, if applicable, mortgage insurance (PMI). Additionally, homeowners pay for monthly utilities and sometimes homeowners association (HOA) fees, which should also be factored into your budget. Our mortgage calculator includes these typical monthly costs to help you accurately crunch the numbers.

Formula for calculating monthly mortgage payments:

The easiest way to calculate your mortgage payment is to use a calculator. However, for the curious or mathematically inclined, here’s the formula for calculating principal and interest yourself:

Where:

- M is monthly mortgage payments

- P is the principal loan amount (the amount you borrow)

- r is the monthly interest rate

(annual interest rate divided by 12 and expressed as a decimal)- For example:

- if the annual interest rate is 5%,

- the monthly rate would be

0.05 / 12 = 0.00417, or 0.417%

- n is the total number of payments in months

- For example:

- for a 30-year loan, n =

30 × 12 = 360months

Here’s a simple example:

This formula assumes a fixed-rate mortgage, where the interest rate remains constant throughout the loan term. Remember to add taxes, insurance, utilities, and HOA fees, if applicable, to get the full picture of your monthly costs.

Play with different home prices, locations, down payments, interest rates, and mortgage lengths to see how they impact your monthly mortgage payments.

Increasing your down payment and decreasing your interest rate and mortgage term will lower your monthly payment. Taxes, insurance, and HOA fees vary by location. If your down payment is less than 20%, PMI costs will be added. We also include a utilities estimate you can break down by service. Add HOA fees if you’re buying a condo or in a community with an HOA.

We haven’t included savings for home maintenance/repairs or home improvement costs. To see how much home you can afford with these costs, check out the Kambia home affordability calculator.

Fun fact: Property tax rates are very localized. Homes of similar size and quality on either side of a municipal border can have different tax rates. Buying in an area with a lower property tax rate may help you afford a higher-priced home.

Includes Taxes and Insurance

Our mortgage calculator shows your payments with property taxes and homeowners insurance included. These costs are often rolled into your monthly mortgage payments to ensure they stay current, protecting your investment and satisfying lender requirements.

• Property Taxes: Fund local services like schools, roads, and police. Even after paying off your mortgage, property taxes remain a responsibility.

• Homeowners Insurance: Required by lenders while you have a mortgage to protect the property. Once your mortgage is paid off, maintaining insurance is optional but recommended for protection against damages.

Calculates Mortgage Costs with PMI

Private mortgage insurance (PMI) helps you qualify for a mortgage without a 20% down payment. Opting for a lower down payment with PMI allows you to buy a home sooner and keep cash for future needs.

• PMI Removal: Automatically removed from conventional mortgages once home equity reaches 22%. You can also request removal when you reach 20% equity.

Includes HOA Fees

Our calculator factors in homeowners association (HOA) fees, which are common with condos, townhomes, and planned developments.

• HOA Fees: Cover maintenance of shared structures and amenities. They typically increase annually and may include special assessments for unexpected expenses.

Using my mortgage calculator, you can get a comprehensive view of your total mortgage costs, helping you make informed financial decisions.

The lower the home price, the lower your loan amount will be. If the seller won’t negotiate, consider these options:

Extend the Length of Your Mortgage

Increasing your loan term, such as choosing a 30-year mortgage over a 15- or 20-year term, will reduce your monthly payments.

Increase Your Down Payment

A larger down payment reduces your loan amount and monthly payments. Putting down at least 20% avoids PMI (private mortgage insurance). Even a 5% increase in your down payment can lower PMI fees.

Get a Lower Interest Rate

A higher down payment can help you qualify for a lower interest rate by improving your loan-to-value ratio (LTV). Consider buying points to lower your rate if you plan to stay in your home for a while. For shorter stays, an adjustable-rate mortgage (ARM) offers a lower initial rate for a set period before adjusting.

Improving your credit score and reducing your debt-to-income ratio (DTI) can also increase your chances of securing a lower interest rate.

The easiest way to know if a home is in your budget is with a calculator! Try our home affordability calculator. Just enter your income, savings, and a few other details, and it will tell you the maximum amount of home you can afford.

What is the principal of a loan?

The principal of a loan is the remaining balance of the money you borrowed, not including the interest, which is the cost of the loan.

What is a down payment?

The down payment is the money you pay upfront to purchase a home. The down payment plus the loan amount should equal the cost of the home. Use Kambia’s down payment assistance page and questionnaire tool to find assistance programs you may qualify for.

APR vs interest rate?

The interest rate is the base fee for borrowing money, while the annual percentage rate (APR) includes the interest rate plus lender fees. APR provides a more accurate idea of the total cost of a financing offer, showing the relationship between the rate and fees.

How much are closing costs?

Closing costs for a home buyer typically range from 2% to 5% of the home’s purchase price. Depending on the loan type, these costs may be included in the mortgage payment or paid at closing. Agent commission is usually paid by the seller.

How much is private mortgage insurance?

The cost of private mortgage insurance (PMI) varies based on factors like credit score, down payment, and loan type.

How much is homeowner’s insurance?

You should consult with your insurance carrier, but generally, homeowner’s insurance costs around $35 per month for every $100,000 of the home’s value.