Buying a home is exciting, but figuring out how much you can afford involves several key factors. Let’s break it down:

Upfront Costs vs. Monthly Costs

Consider both one-time upfront costs and ongoing monthly expenses. Upfront costs include your down payment and closing costs. Monthly costs cover mortgage payments, property taxes, insurance, and utilities. Balancing these is crucial for determining your budget.

| Upfront costs include | Monthly costs include |

|---|---|

| Down payment | Mortgage payments |

| Closing costs | Property taxes |

| Appraisal fee | Homeowners insurance |

| Home inspection | Mortgage insurance |

| Escrow fees | Homeowners association fees |

| Moving costs |

Income

Your income plays a significant role in affordability. Lenders look at your debt-to-income ratio (DTI) to assess how much you can borrow.

- Higher income: Allows a higher DTI and more budget flexibility.

- Lower income: Limits borrowing capacity and requires careful budgeting.

Debt-to-Income Ratio (DTI)

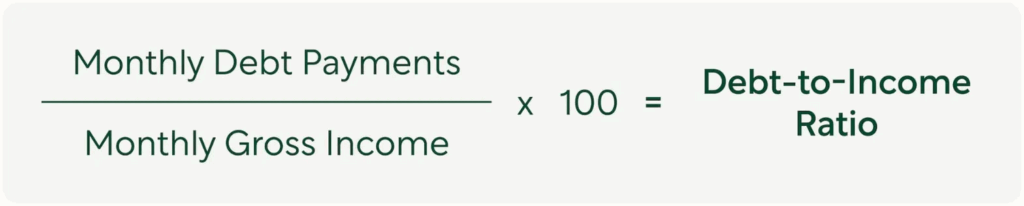

DTI compares your total monthly debt payments to your gross monthly income. Lenders use this ratio to gauge your ability to manage mortgage payments. A lower DTI indicates better financial health and improves your chances of getting favorable loan terms.

- Calculation: Divide monthly debt payments by gross monthly income and multiply by 100. E.g., $2,400 in debt payments and $8,000 in income equals a 30% DTI.

Credit Score

Your credit score affects your loan options and interest rates.

- Good credit: Opens more loan options and lower rates.

- Lower credit: May require a larger down payment, higher interest rate, or PMI.

Improving your credit score can significantly boost your home affordability.

Down Payment

Your down payment impacts your loan amount and monthly payments. Typical down payments range from 3% to 20%.

- Higher down payment: Lowers your loan amount and monthly payments, potentially securing a better interest rate and avoiding PMI.

- Lower down payment: Options like FHA or VA loans can help with limited funds.

Interest Rate

Your interest rate affects your monthly mortgage payments and overall cost.

- Higher rate: Increases monthly payments and total loan cost.

- Lower rate: Decreases monthly payments, making a higher-priced home more affordable.

Factors influencing your rate include the market, credit score, loan amount, and term.

Your income is key in determining how much house you can afford. Lenders use it to calculate your debt-to-income ratio, which shows your ability to make monthly mortgage payments. A higher income means you can afford a more expensive home.

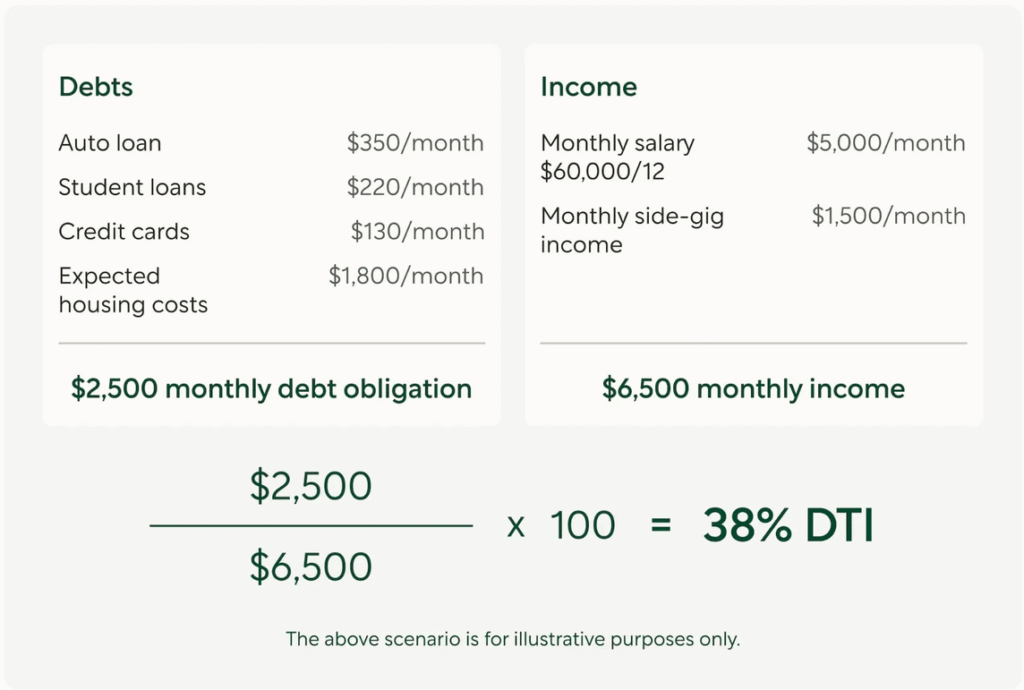

Your debt-to-income ratio (DTI) is crucial in determining how much house you can afford. Lenders use DTI to assess your ability to manage additional debt. A lower DTI means you can afford more, while a higher DTI suggests payment challenges. Keeping your DTI within the acceptable range is essential.

Formula for calculating your debt-to-income (DTI) ratio

Here’s an example of what calculating your DTI might look like

Your credit score tells lenders how reliable you are with credit and impacts the interest rate you get. A higher score can get you lower rates, making it possible to afford a pricier home. On the other hand, a low score might lead to higher rates or even rejection of your mortgage application.

Your down payment is crucial in determining how much house you can afford. It’s the upfront amount you pay at closing, typically ranging from 3% to 20% of the sale price. A larger down payment lowers your mortgage balance, reduces your monthly payments, and may even get you a lower interest rate, helping you afford a more expensive home.

Your mortgage interest rate is key in determining how much house you can afford. A higher rate means higher monthly payments, reducing your mortgage amount. Conversely, a lower rate can increase your purchasing power, letting you afford a more expensive home. Your rate directly affects your monthly budget and homeownership options.

Lenders evaluate factors like income, debt, expenses, credit score, and payment history to determine how much house you can afford. They use financial ratios to assess your ability to repay the loan and consider your overall financial stability and creditworthiness.

To determine your monthly mortgage payment, use your debt-to-income ratio (DTI) as a guide. Ideally, your mortgage payment and other recurring debts should not exceed 50% of your monthly income. It’s also wise to have a cushion of 3-6 months’ worth of savings for unexpected expenses or changes in income.

Other online calculators use general rules of thumb to estimate how much house you can afford, like “never spend more than 43% of your income on a mortgage.”

We do things differently. Our home affordability calculator uses your information, checks the latest interest rates, and runs a quick automated underwriting process. This considers thousands of loan products and rates available to our borrowers, providing accurate estimates to give you the best insight into your buying power.

#1: Check Your Cash Flow

First, see how a new mortgage fits into your budget. Look at your income and expenses honestly. If needed, find ways to earn more or spend less.

#2: Consider All Costs

A mortgage is more than just a monthly payment. Include upfront and ongoing costs like your down payment, closing costs, principal, interest, property taxes, and homeowner’s insurance. Don’t forget about PMI or HOA fees if applicable.

#3: Improve Your Financial Profile

Strengthen your finances before applying for a mortgage. Pay off debt, boost your credit score, and save more for a down payment. A first-time homebuyer course can help you develop a strategy.

#4: Explore Mortgage Options

There are many types of mortgage loans. Look into conventional mortgages, FHA loans, and government-backed options like VA or USDA loans. First-time homebuyer resources can also reduce upfront costs and help you qualify.

#5: Choose a Manageable Home

Homeownership means handling repairs and maintenance yourself. Beyond upfront costs and mortgage payments, be ready for repairs, upgrades, and furnishing your home. Buy a house you can afford to maintain.

#6: Stick to Your Budget

The home-buying process can be emotional. You might fall in love with a home and get outbid. Stay strong and stick to your budget to avoid struggling with mortgage payments. Our mortgage calculator can help you avoid borrowing too much.